1. Europe Date Sugar Market Overview – Definition, scope, and significance?

Date sugar is a natural sweetener derived from the fruit of the date palm, processed into granules, powdered form, or syrup. In Europe, the market encompasses all commercial activities related to the production, distribution, and consumption of date‑based sweeteners across retail, food‑service, and industrial sectors. The scope includes both organic and conventional varieties and spans a wide range of end‑uses such as bakery, confectionery, snacks, dressings, condiments, sauces, and spreads. The significance of the market lies in its alignment with growing consumer demand for clean‑label, low‑glycemic, and plant‑based ingredients, positioning date sugar as a strategic alternative to refined cane or beet sugar.

2. Europe Date Sugar Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include heightened health consciousness, the “no‑added‑sugar” trend, and the rise of organic food retail channels. European regulations that favor natural sweeteners over synthetic alternatives further boost demand. Restraints stem from higher production costs compared with conventional sugar and limited awareness among traditional bakers. Challenges involve supply‑chain constraints for high‑quality dates and the need for consistent product specifications across granules, powdered, and liquid forms. Opportunities arise from product innovation (e.g., fortified date‑sugar blends), expansion into premium “functional food” categories, and increasing online retail penetration that can reach niche health‑focused consumers.

3. Europe Date Sugar Market Growth Trends – Current and emerging trends shaping the market?

Current trends show a shift from bulk conventional sugar to specialty sweeteners, with date sugar gaining traction in artisan bakeries and vegan confectionery. Emerging trends include the launch of organic‑certified date‑sugar lines, the development of low‑calorie syrup variants, and the integration of date sugar into dairy‑free sauces and spreads. The market is also witnessing a trend toward “dual‑segment” products that combine granules for texture with powdered forms for solubility, catering to both home cooks and industrial manufacturers.

4. COVID-19 Impact on the Europe Date Sugar Market – Pandemic effects and recovery trajectory?

The pandemic initially disrupted logistics for raw dates, causing short‑term inventory shortages. However, the shift toward home cooking and increased online grocery sales accelerated awareness of natural sweeteners. By late 2021, the market rebounded strongly, and the recovery trajectory remains positive, supported by sustained consumer interest in healthier pantry staples. The post‑COVID environment has reinforced the resilience of the date‑sugar segment, positioning it for continued growth.

5. Europe Date Sugar Market Competitive Landscape – Major competitors and market consolidation?

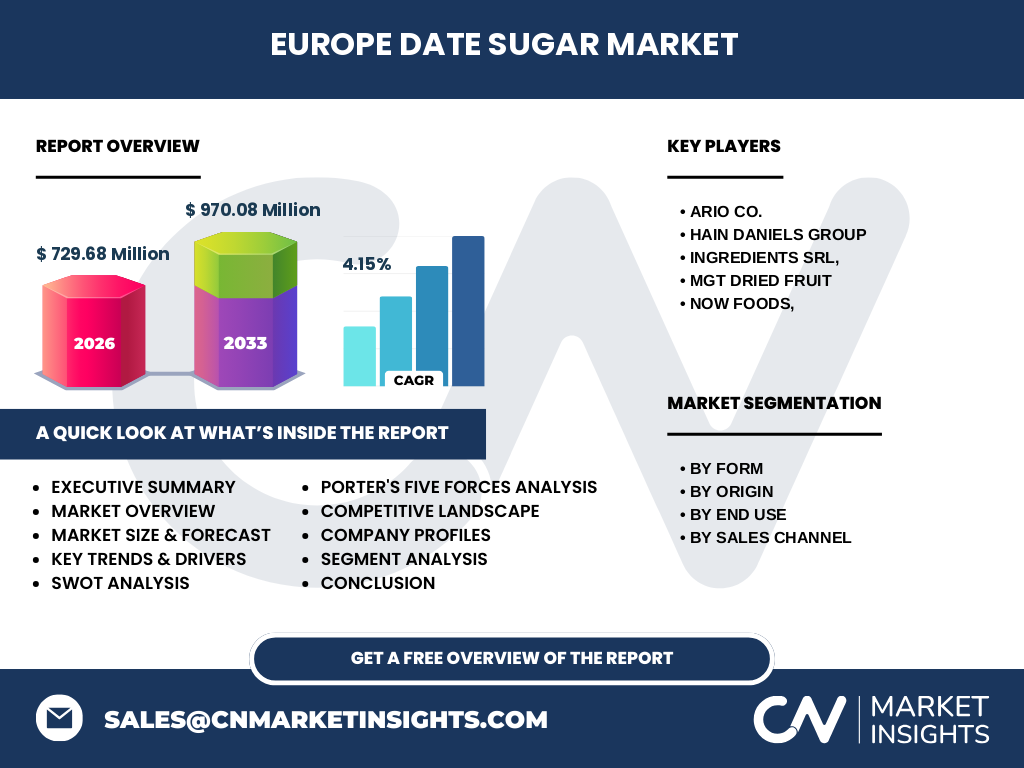

The competitive arena is led by a mix of established food‑ingredients players and niche specialty manufacturers. Key companies include Ario Co., Hain Daniels Group, Ingredients srl, MGT Dried Fruit, and NOW Foods. These firms compete on product differentiation (organic vs. conventional), form factor (granules, powder, syrup), and channel strategy (supermarket private labels versus specialty stores). Recent years have seen modest consolidation through strategic partnerships rather than large‑scale mergers, allowing companies to expand geographic reach while maintaining distinct brand identities.

6. Executive Summary – High‑level overview and key findings about Europe Date Sugar Market?

The Europe Date Sugar Market was valued at €729.68 million in 2026 and is projected to reach €970.08 million by 2033, reflecting a CAGR of 4.15 % over the forecast horizon. Growth is driven by health‑focused consumer trends, expanding organic channels, and versatile end‑use applications. The market is segmented by form (granules & crystal, powdered, syrup/liquid), origin (organic, conventional), end‑use, and sales channel. Competitive dynamics are characterized by a handful of specialized players leveraging product innovation and distribution diversification. Opportunities abound in functional‑food development and digital retail.

7. Europe Date Sugar Market Forecast – Projections for 2025‑2032 period?

Based on the provided CAGR of 4.15 %, the market is expected to maintain steady expansion from the 2026 base of €729.68 million to approximately €970.08 million by 2033. This trajectory suggests incremental annual growth of roughly €30‑€35 million, reflecting continued demand across bakery, confectionery, and premium sauce segments. The forecast assumes stable macro‑economic conditions in Europe, ongoing consumer preference for natural sweeteners, and no major supply disruptions.

8. Europe Date Sugar Market Size and Share by Segmentation – Breakdown by segment?

By Form, the market is divided into Granules & Crystal, Powdered, and Syrup/Liquid. Granules & Crystal dominate the bakery and snack categories due to their texture, while Powdered forms are preferred in confectionery and sauces for easy dissolution. Syrup/Liquid finds niche use in dressings and beverage formulations. By Origin, organic date sugar commands a premium price and captures the growing “clean‑label” segment, whereas conventional sugar holds the larger volume share due to broader availability. By End Use, bakery leads in volume, followed by confectionery, snacks, dressings & condiments, and sauces & spreads. Finally, Sales Channel analysis shows Hypermarkets/Supermarkets as the primary distribution point, complemented by Specialty Grocery Stores for premium organic lines, and a fast‑growing Online Retail segment.

9. Global Europe Date Sugar Market Size and Share by Region – Geographic distribution?

Within the broader global context, Europe accounts for the largest regional share of the date‑sugar market, driven by stringent food‑label regulations and high consumer health awareness. While exact percentages are not disclosed, the €729.68 million valuation in 2026 underscores Europe’s leading position relative to North America and the Middle East, where market development is still emerging.

10. Regional Analysis of the Europe Date Sugar Market – Detailed regional market performance?

Western Europe (Germany, France, UK, Benelux) shows the strongest demand, propelled by mature retail infrastructure and a sizable organic‑product portfolio. Southern Europe (Spain, Italy, Greece) benefits from proximity to date‑producing regions, resulting in shorter supply chains and competitive pricing for conventional varieties. Scandinavia displays steady growth in the premium organic segment, while Central and Eastern European markets are accelerating adoption through discount‑store channels and increasing awareness of natural sweeteners.

11. Leading Company Profiles in the Europe Date Sugar Market – Industry players and strategies?

Ario Co. focuses on high‑purity powdered date sugar, leveraging proprietary drying technology to ensure consistent solubility. Hain Daniels Group offers a broad portfolio across all three forms, emphasizing private‑label partnerships with major hypermarket chains. Ingredients srl differentiates through certified organic granules targeting specialty grocery retailers. MGT Dried Fruit supplies both conventional and organic syrup, positioning itself as a key ingredient for dressings and sauces. NOW Foods integrates date sugar into its health‑focused product line, promoting functional benefits through nutritional labeling.

12. Porter's Five Forces Analysis of the Europe Date Sugar Market – Competitive forces assessment?

Threat of New Entrants: Moderate. Entry barriers include expertise in date processing and certification for organic status. Bargaining Power of Suppliers: High, due to limited sourcing regions for premium dates. Bargaining Power of Buyers: Moderate to high, especially large retail chains that can negotiate volume discounts. Threat of Substitutes: Moderate, with alternatives such as stevia, erythritol, and traditional sugar competing on price and functionality. Industry Rivalry: Intense, driven by product innovation and channel diversification among the leading five players.

13. SWOT Analysis of the Europe Date Sugar Market – Strengths, weaknesses, opportunities, threats?

Strengths: Natural, low‑glycemic profile; alignment with clean‑label trends; versatile applications across food categories.

Weaknesses: Higher cost compared with refined sugar; limited raw‑material supply; variable consumer awareness.

Opportunities: Expansion into functional‑food lines; growth of organic and online retail channels; development of fortified or flavored date‑sugar blends.

Threats: Price volatility of raw dates; competitive pressure from low‑cost sweeteners; potential regulatory changes affecting labeling claims.

14. Europe Date Sugar Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with date cultivation in North Africa and the Middle East, followed by procurement, cleaning, and dehydration. Next, processing facilities convert dates into granules, powder, or syrup, applying organic certification where required. Distribution channels include bulk shipments to European ingredient distributors, who then supply manufacturers (bakery, confectionery, sauces) and retail packagers. Final sales occur through hypermarkets, specialty stores, discount outlets, and online platforms. Value‑added services such as custom blending and private‑label development are increasingly common among the leading firms.

15. Key Investment Insights in the Europe Date Sugar Market – Strategic investment recommendations?

Investors should prioritize companies with diversified form‑factor portfolios and strong organic certification capabilities, as these address the fastest‑growing consumer segments. Partnerships with Mediterranean date producers can mitigate supply risk and improve cost structures. Funding digital‑commerce capabilities will capture the expanding online retail share. Lastly, R&D investment in functional blends (e.g., fiber‑enriched date sugar) can open new premium markets and command higher margins.

16. Europe Date Sugar Market Conclusion – Summary and key takeaways?

The Europe Date Sugar Market is on a solid growth path, underpinned by health‑centric consumer preferences and a robust €729.68 million base in 2026. A 4.15 % CAGR to €970.08 million by 2033 reflects steady adoption across multiple food categories and sales channels. Success hinges on supply‑chain resilience, organic differentiation, and strategic channel expansion, especially online. Companies that innovate in product form and functional benefits are positioned to capture the most value.

17. Research Methodology – How this research was conducted?

The study combines primary interviews with industry experts, supply‑chain participants, and key retailers, together with secondary data from company reports, trade publications, and government statistics. Market sizing utilizes a top‑down approach anchored on the provided 2026 valuation and forecasted growth rate. Segmentation analysis draws on product‑form, origin, end‑use, and channel data supplied by respondents and corroborated by public sources.

18. Research Scope – Coverage and limitations?

The scope covers the European geographic region, encompassing all commercial activities related to date‑derived sweeteners across the defined forms, origins, end uses, and sales channels. The analysis excludes unrelated date‑fruit products (e.g., whole dried dates) and does not quantify market share beyond the aggregate size and growth figures provided. All financial figures are based on the explicit data supplied.

19. Key Companies and Recent Developments in the Europe Date Sugar Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Ario Co. launched a new high‑solubility powdered date sugar aimed at the beverage sector in early 2024. Hain Daniels Group announced a strategic partnership with a Moroccan date cooperative to secure a 5‑year supply of organic raw dates, enhancing its private‑label granule line. Ingredients srl introduced an organic granule blend fortified with vitamin B12 for the health‑food market. MGT Dried Fruit rolled out a low‑calorie syrup variant, marketed to sauce manufacturers seeking reduced sugar content. NOW Foods expanded its functional range with a “Superfood Date Sugar” product, emphasizing antioxidant content and targeting online health‑consumer platforms.